What Led to The Collapse of Silicon Valley Bank? And What Could Be The Ripple Effects?

- Stay Informed With Sanil | Sanil Pinto

- Mar 11, 2023

- 4 min read

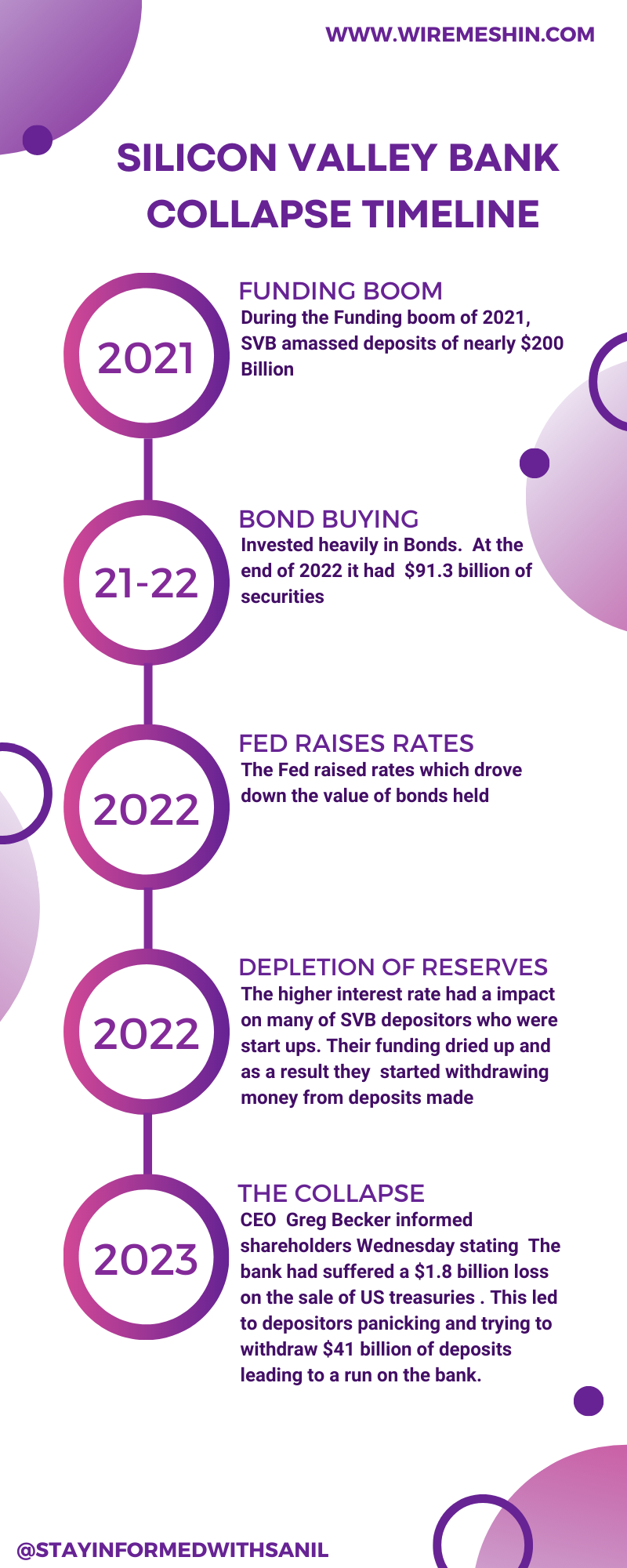

Silicon Valley Bank, the financial institution known for its relationships with high-flying world technology startups and venture capital, experienced one of the oldest problems in banking, a bank run, which led to its failure on Friday. The bank's downfall is the largest failure of a financial institution since Washington Mutual collapsed at the height of the financial crisis more than a decade ago. The bank was hit hard by the downturn in technology stocks over the past year as well as the Federal Reserve's aggressive plan to increase interest rates to combat inflation. The bank bought billions of dollars worth of bonds over the past couple of years, using customers' deposits as a typical bank would normally operate. These investments are typically safe, but the value of those investments fell because they paid lower interest rates than what a comparable bond would pay if issued in today's higher interest rate environment.

Silicon Valley's customers were largely startups and other tech-centric companies that started becoming more needy for cash over the past year. Venture capital funding was drying up, companies were not able to get additional rounds of funding for unprofitable businesses, and therefore had to tap their existing funds, often deposited with Silicon Valley Bank, which sat in the center of the tech startup universe. So Silicon Valley customers started withdrawing their deposits. Initially, that wasn't a huge issue, but the withdrawals started requiring the bank to start selling its own assets to meet customer withdrawal requests. Because Silicon Valley customers were largely businesses and the wealthy, they likely were more fearful of a bank failure since their deposits were over $250,000, which is the government-imposed limit on deposit insurance. That required selling typically safe bonds at a loss, and those losses added up to the point that Silicon Valley Bank became effectively insolvent.

Silicon Valley Bank Chief Executive Officer Greg Becker sent a letter to shareholders on Wednesday stating the bank had suffered a $1.8 billion loss on the sale of US treasuries and mortgage-backed securities and outlined a plan to raise $2.25 billion of capital to shore up its finances. This letter resulted sent investors in panic and depositors tried to pull $42 billion from Silicon Valley Bank on Thursday. At the close of business on March 9, the bank had a negative cash balance of $958 million, according to an order taking possession of the bank filed Friday by California’s bank regulator, the Department of Financial Protection and Innovation. The scale of attempted withdrawals was so large that the bank ran out of cash and ways to get it. When the Federal Reserve sent its cash letter — a list of checks and other transactions for the bank to process - to SVB, it failed to pull together enough currency to meet it, according to the California regulator. “Despite attempts from the bank, with the assistance of regulators, to transfer collateral from various sources, the bank did not meet its cash letter with the Federal Reserve,” the order from Commissioner Clothilde Hewlett said.

The most immediate problem is Silicon Valley Bank's large deposits. The Federal government insures deposits to $250,000, but anything above that level is considered uninsured. The vast majority of Silicon Valley Bank's deposits were uninsured, a unique characteristic of the bank due to its customers being largely startups and wealthy tech workers. At the moment, all of that money can't be accessed and likely will have to be released in an orderly process. But many businesses cannot wait weeks to get access to funds to meet payroll and office expenses. It could lead to furloughs or layoffs.

The bank regulators had no other choice but to seize Silicon Valley Bank's assets to protect the assets and deposits still remaining at the bank. However, experts don't expect the issues to spread to the broader banking sector. Silicon Valley Bank was large but had a unique existence by servicing nearly exclusively the technology world and VC-backed companies. It did a lot of work with the particular part of the economy that was hit hard in the past year. Other banks are far more diversified across multiple industries, customer bases, and geographies.

In conclusion, Silicon Valley Bank's collapse is not the same as the 2008 financial crisis. Silicon Valley Bank was unique in its existence by servicing nearly exclusively the technology world and VC-backed companies. The bank's collapse was caused by a bank run and other factors such as the downturn in technology stocks over the past year and the Federal Reserve's aggressive plan to increase interest rates to combat inflation. While there will be economic ripple effects in technology startup world if the remaining money can't be released quickly, experts don't expect the issues to spread to the broader banking sector. Let’s do hope that’s really the case.

Don't forget to leave your comment and Like and Share this article if you found this is useful and important to You or family and friends!

If you have any questions on personal finance and Investing leave a message on any of the below mediums and we will help give wings to your financial dreams.

@stayinformedwithsanil | www.wiremeshin.com

Comments